QQ登录

QQ登录 微博登录

微博登录 微信登录

微信登录

ACCA考试科目F5超全知识点总结!高顿学姐收集的一些学霸知识点总结,推荐大家仔细阅读!希望对你的A考有所帮助!

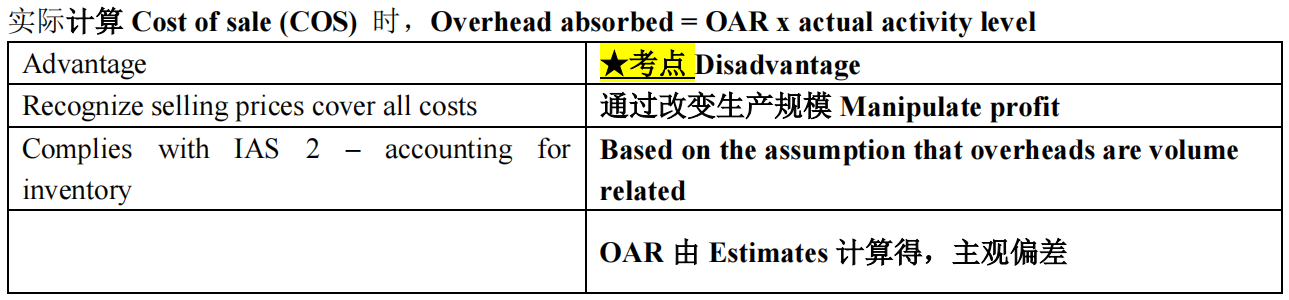

一、Absorption costing

OAR=Estimated Production Overhead/Estimated Activity Level,都是budget值。Activity level可以是production units,可以是labor hours,也可是machine hours,取决于劳动密集,还是机械生产密集intensive。

二、Marginal costing

1.Advantage

适合decision making as it highlights contribution

Fixed cost are treated as period costs

Profit depends on sales and efficiency

2.Disadvantage

Danger that products sold on marginal contribution-fail to cover fixed costs

Doesn't comply with IAS 2,需要调整报表

Necessitates analysis of mixed costs between FC andVC

★技巧

AC=MC+(Closing Inventory-Opening Inventory)x OAR

AC=MC+(Closing Inventory-Opening Inventory)x OAR

The absorption costing requires subjective judgments.预算估计主观判断太多

There is often more than one way to allocate the overheads.制造成本分摊可操纵

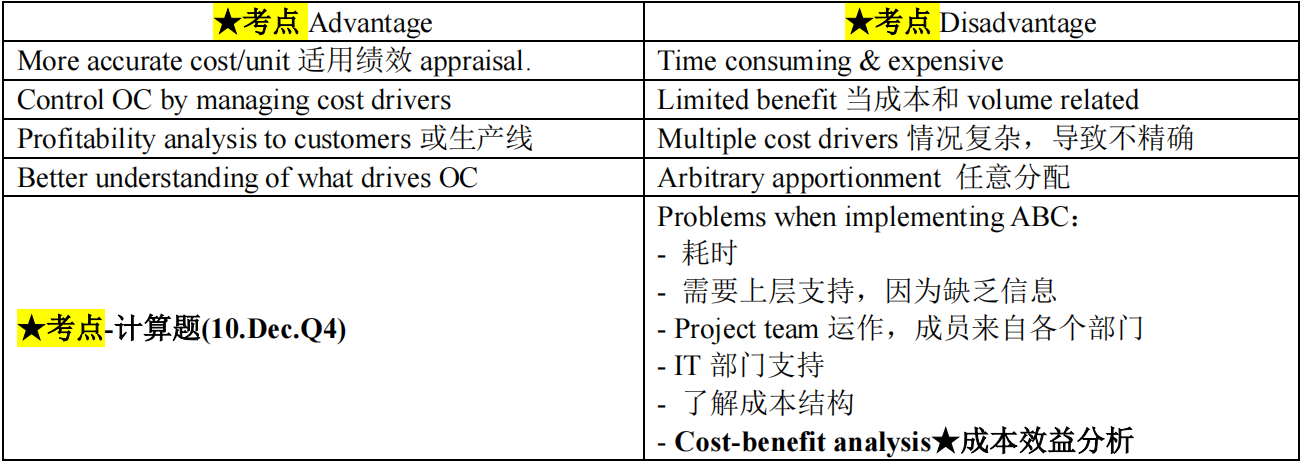

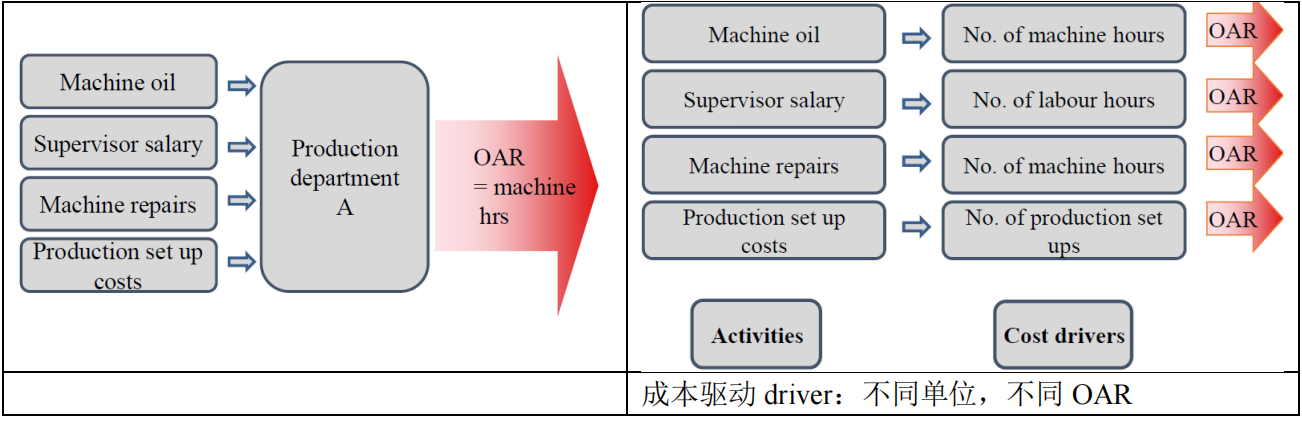

三、Activity-based costing

三、Activity-based costing

解题步骤:Cost Pool → Cost Drive →OAR→Absorbed →Full Cost