QQ登录

QQ登录 微博登录

微博登录 微信登录

微信登录

随着2018年第二个考试窗口的关闭,很多学员已经开始准备第三个考试窗口的考试了。

为了让大家更好的掌握AICPA官网推出的7月份考纲更新,小编特意为大家详细列举了每科的考试变化更新内容。

考纲具体变化内容在《Uniform CPA Examination BLUEPRINTS(Effective Date July.1,2018)》和《Summary of revisions to the Uniform CPA Examination Blueprints(Effective Date July.1,2018)》中有详细介绍

今天先为大家整理了AUD科目的更新内容。满满干货,往下翻~!

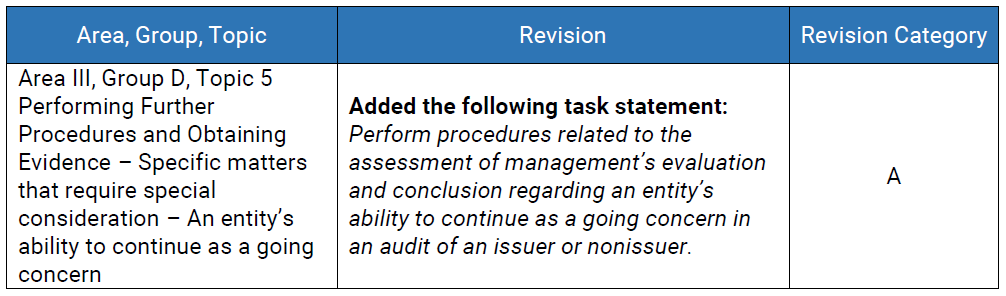

1.Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern

考纲变化:反映SAS No.132(AU-C 570 The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern):在Performing Further Procedures and Obtaining Evidence阶段,增加Specific matters that require special consideration–An entity’s ability to continue as a going concern;

考纲解读:相当于考试对going concern问题增加了一个考点,以前爱考针对going concern发表不同意见,现在多了一个考点——审计师对企业的going concern进行测试和评估

补充学习:The objectives of the auditor are as follows:

To obtain sufficient appropriate audit evidence regarding,and to

conclude on,the appropriateness of management's use of the going

concern basis of accounting,when relevant,in the preparation

of the financial statements

To conclude,based on the audit evidence obtained,whether substantial

doubt about an entity's ability to continue as a going concern

for a reasonable period of time exists

To *uate the possible financial statement effects,including the

adequacy of disclosure regarding the entity's ability to continue

as a going concern for a reasonable period of time

To report in accordance with this section

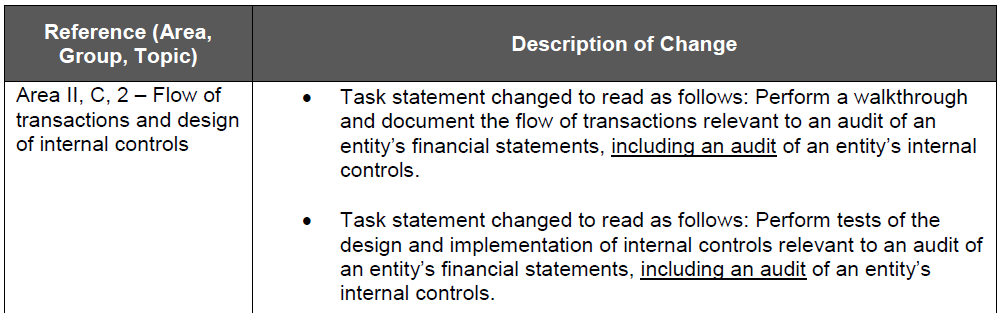

2.Audit of Internal Control Over Financial Reporting

考纲变化:反映SAS No.130(AU-C 940 An Audit of Internal Control Over Financial Reporting[ICFR]That Is Integrated With an Audit of Financial Statements)的术语变化,将“an examination of entity's internal controls"统一改成”An audit of entity's internal controls"

考纲解读:此点变更仅是术语变化,为了对财务报表内部控制的审计,与财务报表审计能更好地结合,考试基本不会受到影响。

3.New Reporting Standards Issued by PCAOB

官方通知(非考纲变化):会对PCAOB发布的new reporting standards进行考核,具体时间是除了Critical Audit Matters(CAM)的其他内容从2018年7月以后考核,CAM相关内容从2019年7月以后考核。

解读:学员应当加强这部分针对上市公司审计报告准则的学习,但是今年的考纲暂时没有涉及这里,推测今年下半年考试碰到的几率不大,会是明年审计考试的“重头戏”。

补充学习:critical audit matters

Relates to accounts or disclosures that are material to the financial statements,and Involved especially challenging,subjective,or complex auditor judgment

Factors the auditor should take into account in determining CAMs:

a.The auditor's assessment of the risks of material misstatement,including significant risks;

b.The degree of auditor judgment related to areas in the financial statements that involved the application of significant judgment or estimation by management,including estimates with significant measurement uncertainty;

c.The nature and timing of significant unusual transactions and the extent of audit effort and judgment related to these transactions;

d.The degree of auditor subjectivity in applying audit procedures to address the matter or in *uating the results of those procedures;

e.The nature and extent of audit effort required to address the matter,including the extent of specialized skill or knowledge needed or the nature of consultations outside the engagement team regarding the matter;

f.The nature of audit evidence obtained regarding the matter.

填写下面表单,领取2018年AICPA大礼包一份!